If I’m being honest—I don’t like the word financial. Silly right?

When I read the word “financial”, it conveys far more treacherous meaning than, “related to finance” or “related to the management of money”.

For me, this word carries woeful connotations attributed to having graduated college during the Global Financial Crisis of 2007-2008.

When I think—financial—I instantly marry it with other words such as financial: ruin, despair, setbacks, hardships, turmoil, and so on and so forth.

All of these sound like a match made in hell. 😈

Two primary reasons are why this happens:

- I had a rocky start with my own finances after college.

- I’ve been conditioned to form negative associations with this word.

As of writing this, typing the word financial into Google and clicking the News tab returns these results:

“Financial Problems Bigger Than Personal Issues”

“Former NSA Chief Warns of Russian Cyberattacks against US Financial Sector”

“Europe faces ‘severe’ risk of disorderly financial market correction”

“Past financial crisis have made millennials ‘more cautious, more proactive’ in how they manage money ” (that’s for darn sure).

In my opinion, this word stinks, and as much as I’ll reluctantly use it, I didn’t in the title of this blog post which should have been: “The Basics of Financial Planning” or something dull to that effect.

Instead, I decided to call this article, “Intro to Money Mastery”, because at least for me, the word “money” elicits feelings of happiness—I mean who doesn’t like money? 😊

Speaking of the post title, I assume you’re working and making your own money.

Good.

I also assume that you have a general idea of how to manage your money—let’s build off that.

For starters, we want to earn more money than we spend.

Obvious? I guess for a lot of us no:

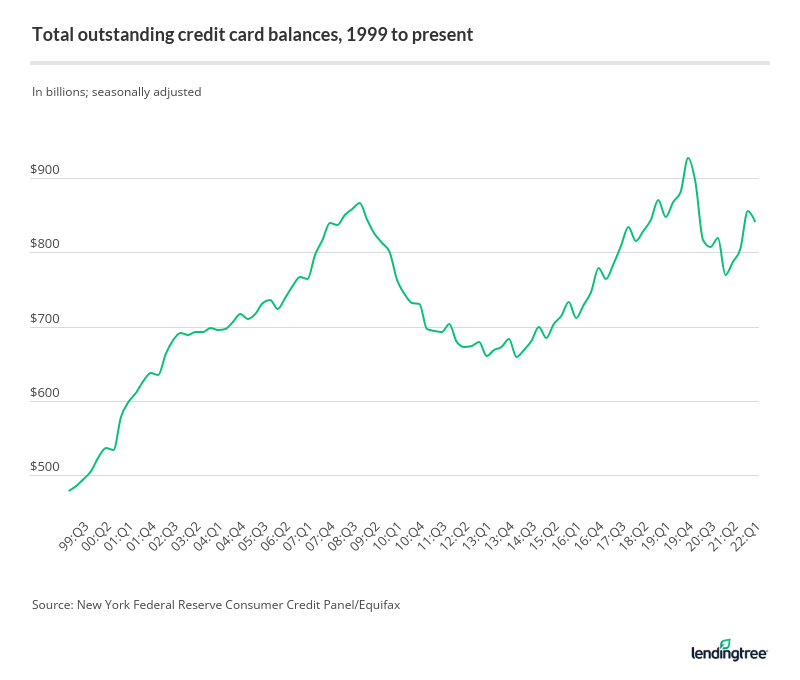

You don’t have to be a data wonk to behold Jacob’s laddah ovah’ here.

You don’t have to be a data wonk to behold Jacob’s laddah ovah’ here.

This graph depicts an alarming phenomenon—that Americans from coast to coast are saddling up the debt.

Let’s say I rake in a net income of 2 grand a month. After the bills are paid I’m left with 300 bucks—not bad.

The thing is, there’s this espresso machine I saw online that’s got a chokehold on me. Not only does it look bougie as hell, but it grinds, doses, and extracts. And that bean hopper capacity—my goodness—I’ll be wired like a server rack!

I will literally lose it if I don’t hear me some dank roast dribbling by Monday morning.

The flip side is that it costs an exorbitant 800 dollars.

Well, I have just the rationale to justify a senseless purchase like this:

According to Experian, the average credit card balance is $5,525 per household.

According to Experian, the average credit card balance is $5,525 per household.

The Basics of Financial Planning

Financial planning just means managing the money you’re bringing home and yes, it involves a plan.

A plan doesn’t exist without an end game—there has to be goals.

Where there are goals, there also must be strategies to achieve those goals.

Absent a plan, you’re just haphazardly throwing your cash all over the shop; paying bills on the fly, spending blindly, and relying on mental math to confirm you’ll have rent money left over after a night out with pals.

Speaking plainly—that’s just stupid.

Preparing Your Financial Plan

The time-tested process of financial planning looks like this:

- Explicitly define financial goals

- Develop strategies to achieve said goals

- Execute those strategies

- Evaluate progress

- Revise as needed

It’s worth noting that this general process can be applied to just about any plan—financial or not—but as far as your finances are concerned, trust the process and don’t look back.

This is the way.

Defining Your Financial Goals

The first step in financial planning is to clearly state your goals.

Here are a few general examples of financial goals to help you contemplate your own:

- Pay off debt

- Build and emergency fund

- Purchase a home

- Reduce expenses by 15%

- Buy a car

- Save for a vacation

- Buy a new TV

- Find a better paying job

You absolutely must take into account your current financial situation when deciding your goals. If you’re asking yourself what goals make the most sense for you, read this post.

As you’re brainstorming, do what I do—take out a notebook and write them down. By writing them down, the ball starts to roll.

One of the hardest parts of doing anything is to overcome the inertia of actually doing it. At least jotting your goals offers little resistance, and you’ll find it easier to hit your stride as you progress.

Realistic or Just Pessimistic?

It’s important that your goals are realistic.

Again, being realistic about your goals just means taking stock of your current financial situation and planning feasible outcomes within a specified time frame.

Real quick—if I’m netting 50k a year, driving a Lambo fresh off the lot by the year’s end would not be a realistic goal. You get it—I know—but what if I really did want a supercar?

Well, I’m not in the business of discouraging any financial goals because they’re too lofty, ambitious, or what some would call extravagant.

The Prosper Mentality dictates that anything in life is possible, but what I am saying is that for now, before you’re all comfortably nestled in the lap of luxury, start planning realistically to lay the groundwork for more aspiring goals in the near future.

Good Things Take Time

A well-rounded financial plan consists of short-term, intermediate-term, and long-term goals.

- Short-term—one year or less (e.g., buying: furniture, TV, appliances)

- Intermediate-term—one through five years (e.g., pay off a loan)

- Long-term—five plus years (e.g., retire)

You’ll find that upon completing your financial plan, the timing of several of your goals will fall into either of these three buckets.

Tacking on a date to your financial goals is essential.

Having a concrete date hold us accountable and ensures that we’re on track with our goals.

Develop Strategies

The word strategy has an interesting etymology. It derives from the Greek word, ‘strategos’, meaning general or commander of an army.

For the most part, a general’s not worried about being carted off the front lines in the meat wagon. The General, and the other top brass are too busy hunched over a dimly lit map sliding pieces around like seasoned croupiers.

A general without a plan will never triumph in wartime.

The general is the master architect. When building your financial plan, you are also the general—the master architect of your money.

The General’s Map

Imagine that you are now dubbed, “General Wherewithal”.

Opposite you lies a tabletop map demarcated by four different territories: spending, saving, investing, retirement, and insurance.

A humble pile of glimmering, brass dollar sign tokens rests on the far corner of the map atop home base—Fort Income—awaiting to be dispatched.

You—General Wherewithal—must now contemplate where to move each individual token.

What do you do?

Your primary zones of movement consist of the following:

- Spending—where your money is going (needs & wants; bills & surround sound systems)

- Saving—stashing the extra dough (rainy day funds and anything else you’re saving towards)

- Investing—where you intend to park your cash to reap the most gains (stocks, crypto, real estate, etc.)

- Retirement—your nest egg

- Insurance—protecting your assets. (home, car, etc.)

Here’s one thing any high-ranking general of Personal Finance knows:

Money earned should constantly be in motion; and not just into the hands of lenders and e-commerce giants.

If you leave your shiny little brass tokens at home base too long, they’ll get tired and rusty—the rest of us recognize this phenomenon as inflation.

You need to send them on a mission to go out and round up more brass tokens for you—these are what are called returns.

Obviously you can’t send them all out chasing returns; then the bills won’t be paid.

Neither should you exhaust your checking account balance in between pay periods for the sake of prodigal pursuits—leave that up to General Spendthrift who’s preordained to suffer a humiliating defeat.

This is why a good general knows that having a solid plan is imperative in achieving success.

A large part of your financial plan is nothing more than deciding how you spend your money and where to move the rest.

Execute Strategies

When I was a kid I was obsessed with wrestling.

One of my favorite wrestlers of all time was Bret “The Hitman” Hart—to this day, still one of my heroes.

Who can forget this theme song:

Budgeting your money, for example, is just one of many aspects of financial planning that requires self-discipline. If you’ve never tried budgeting your money before, you’ll soon learn why.

I wasn’t a fan when I first started, but I’ve learned to enjoy it with time.

Self-discipline has more value to you than motivation or inspiration.

Why?

Because motivation and inspiration are fair-weather friends; they only stick around when times are good.

Self-discipline on the other hand rides with you through thick and thin.

Always look to self-discipline first as your impetus to action—your financial progress depends on it.

Evaluate Progress

Now that you have your financial plan in motion yo absolutely must keep tabs on your progress.

Are you on track to reach your goals with the time specified?

This means nothing more than an unflinching eye towards your budget and some simple number crunching.

Revise As Needed

Apparently this quote is attributed to Earnest Hemingway, although I’m not quite sure he actually said this.

Doesn’t matter though—it’s a boss quote.

Of course I’m not encouraging that anyone plan their finances while intoxicated, but what I am saying is that you shouldn’t spend too much time over analyzing every single detail to the point of stasis.

I like this quote because you can loosely apply it to just about anything.

I like to think it can imply doing something—anything—with a basic understanding, then refining it as you move along.

Many aspects of your financial plan will require tweaking as you progress.